The Insurance Market Cycle: Hard Versus Soft Markets

February 7, 2024

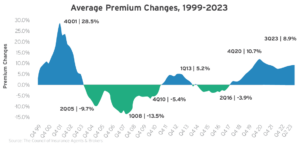

The commercial insurance market is cyclical in nature, fluctuating between hard and soft markets.

These cycles affect the availability, terms and price of commercial insurance, so it’s helpful to know what to expect in both a hard and soft insurance market.

A soft market, which is sometimes called a buyer’s market, is characterized by stable or even lowering premiums, broader terms of coverage, increased capacity, higher available limits of liability, easier access to excess layers of coverage and competition among insurance carriers for new business. On the other hand, a hard market, sometimes called a seller’s market, is characterized by increased premium costs for insureds, stricter underwriting criteria, less capacity, restricted terms of coverage and less competition among insurance carriers for new business.

During a hard market, some businesses may receive nonrenewal notices from their insurance carriers. What’s more, hard market cycles may prompt carriers to stop writing coverage in high-risk locations or even exit certain unprofitable lines of insurance.

Many factors affect insurance pricing, but the following are some of the most common contributors to the hard market:

- Catastrophic (CAT) losses—Floods, hurricanes, wildfires and other natural disasters are increasingly common and devastating. Years of costly disasters like these have compounded losses for carriers, driving up the cost of coverage overall, especially when it comes to commercial property policies.

- Inconsistent underwriting profits—Underwriting profits refer to the difference between the premiums a carrier collects and the money paid out in claims and expenses. When an insurance company collects more in premiums than it pays out in claims and expenses, it will earn an underwriting profit. Conversely, an insurance company that pays more in claims and expenses than it collects in premiums will sustain an underwriting loss. The company’s combined ratio after dividends is a measure of underwriting profitability. This ratio reflects the percentage of each premium dollar an insurance company puts toward spending on claims and expenses. A combined ratio above 100 indicates an underwriting loss.

- Mixed investment returns—Insurance companies also generate income through investments. Commercial insurance companies typically invest in various stocks, bonds, mortgages and real estate investments. Due to regulations, insurance companies invest significantly in bonds. These provide stability against underwriting results, which can vary from year to year. When interest rates are high and returns from other investments are solid, insurance companies can make up underwriting losses through their investment income. But when interest rates are low, carriers must pay close attention to their underwriting standards and other investment returns.

- The economy—The economy as a whole also affects an insurance company’s ability to write new policies. During periods of economic downturn and uncertainty, some businesses may purchase less coverage or forgo insurance altogether. Additionally, a business’s revenue and payroll, which factor into how premiums are set, may decline. This creates an environment where there is less premium income for carriers.

- The inflation factor—Prolonged periods of inflation can make it challenging for insurance carriers to maintain coverage pricing and subsequently keep pace with more volatile loss trends. Unanticipated increases in loss expenses can result in higher incurred loss ratios for insurance carriers, particularly as inflation affects key cost factors (e.g., medical care, litigation and construction expenses).

- The cost of reinsurance—Generally speaking, reinsurance is insurance for insurance companies. Carriers often buy reinsurance for risks they can’t or don’t wish to retain fully. It’s a way for carriers to protect against extraordinary losses. As a result, reinsurance helps stabilize premiums for regular businesses by making it less risky for insurance carriers to write a policy. However, reinsurers are exposed to many of the same events and trends affecting insurance companies and make pricing adjustments of their own.

Thankfully, businesses are not without recourse in the face of a hard market. Business owners who proactively address risk losses and manage exposures will be better prepared for a hardening market than those who do not. Additionally, those who educate themselves on the trends that influence their insurance will better understand how to manage their associated costs. Our Robertson Ryan agents and associates stand ready to support you, contact us today.